In the Real World, Perfect Investing Strategies Don't Exist

When it comes to investing, most people are in search of reliable return streams to facilitate lifestyles and legacies they aspire to. And while we are all unique, we have many things in common in the way we want our money to work for us.

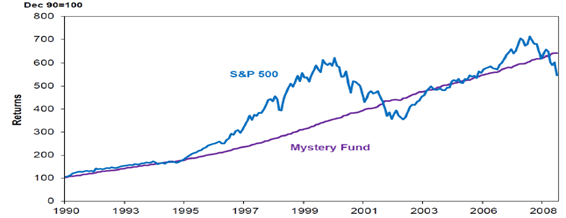

The “perfect” return stream, if we were to sketch it, might resemble the Mystery Fund depicted in the graph below. Specifically, the Mystery Fund has three traits investors covet:

• Safety

• Growth

• Consistency

Safety

You can’t secure your future if you don’t first preserve your past. So the first rule of money management is: don’t lose money.

This does not imply you should take zero risk. Rather, the key is to take measured risk, and contain portfolio drawdown in tumultuous climates.

It helps an investor’s cause immensely to avoid large drawdowns, because higher returns are required to get back to breakeven after experiencing a loss. For instance, losing 25% requires a 33% return to get back to breakeven. Losing 50% requires a subsequent 100% gain to breakeven.

Investors who stand the test of time understand this principle well. There is a market adage: “There are old investors, and there are bold investors, but there are few old bold investors.”

There are also psychological elements to consider. Containing losses is important because of a condition known as ‘loss aversion’—we loath losses proportionately more than we enjoy gains.

The imbalance blurs our ability to rationally navigate markets, and can throw people off track at the wrong time. The last seller who sells a pivotal market bottom does irreparable damage to their long-term return profile.

Growth

In meeting with hundreds of high net worth investors over the years, no one has ever told me their goal was to lose money, or watch it be static. They want growth.

The long-term compounded annual growth rate (CAGR) plays the most critical role in facilitating lifestyle goals. Over the long-term is where compounding exerts huge influence and a wide deviation in investor outcomes.

As a simple illustration of the relationship between compounding and time, suppose I offer to pay you one penny today, with a promise to double it every day for the next month. Two cents tomorrow, and four cents the following day—nothing too exciting. If we stick with the program, however, in 30 days I’m on the hook for over $5 million!

Similarly, a few percent higher CAGR can make a dramatic difference over the course of a typical investor’s time horizon, often spanning several decades. Ben Carlson illustrates that point with the following table:

Consistency

A sound long-term strategy only benefits those who maintain the confidence to stick with it. For this reason, consistency matters.

DALBAR studies of investor behavior show how poor market timing often leads many investors to subpar results. Whatever the caliber of a security or fund, selling low and buying high will always be a recipe for failure.

Investors predilection for performance chasing ties to a behavioral bias known as ‘myopia’—we focus more than we should on short-term performance, even though such results have a minimal impact over a lengthy time horizon.

Selling a great fund or stock after a year of underperformance is like leaving your seat at a baseball game after the first inning, just because the visiting team went up by a run. Silly behavior!

Truly understanding the logic of a strategy helps stay the course when returns suffer.

Relative return consistency is another consideration when designing a portfolio, because our perception of financial well-being is partially shaped by how we deem ourselves to be doing compared to peers. Style diversification—i.e. owning a mix of value and growth securities—is one method that improves relative performance consistency.

Final thought about the Perfect Investment Strategy

Investment managers can spend nights dreaming about perfect investment vehicles, but in the real-world, they don’t exist.

Indeed, pulling back the curtain reveals the “Mystery Fund” manager to be none other than notorious Ponzi schemer, Bernie Madoff!

Yep—that graph is based on his supposed returns.

“If it’s too good to be true, it probably is,” generally holds true with investing. Nevertheless, don’t throw in the towel entirely. Strong risk-adjusted returns are an attainable goal, provided you maintain a clear set of objectives and mindset about what you aim to achieve.