How Warren Buffett Navigates Markets at All-Time Highs

With stocks making all-time highs again, I’m having daily conversations with investors who aren’t sure how to invest their money.

Many ask: Should we put new money to work at these levels, or wait for a pullback?

Others wonder if stocks are in a bubble, which may warrant profit taking.

Warren Buffett recently spoke with "Bloomberg Markets" about his current investing strategy. This isn’t his first rodeo navigating an all-time market high. Click here to watch a 2-minute excerpt of the interview.

Buffett is still among the best in the business at packing a lot of wisdom into just a few minutes of Q&A. Here’s how he answered several important and timely questions, along with extra context provided by me.

***

Question: The stock market is really on a record tear. You’ve always drawn the distinction between price and value. Are we seeing a run up in value, or in price?

Buffett: Value gains from year to year… If you own a business, and you plow back a good portion of your earnings into building the business, you’re going to have something more valuable year after year.

My take: Smart question by the interviewer. What I find interesting about Buffett's response is that he focused more on the value component than price. To me, that indicates he probably doesn’t perceive the stock market to be wildly overvalued. Especially when you compare to the relative yield bonds offer, which he touches on later in his answer.

Buffett describes how earnings growth regularly propels the market’s intrinsic value higher. To help you see that point more clearly, below I have plotted annual earnings growth against the market's annual appreciation.

A few things to note about the graph:

* The rhythm of the market (orange line) correlates with directional shifts in earnings (blue bars).

* The gap between the market and earnings is not as wide this cycle as during the late '90s. That was a bubble. Today's investing environment may be frothy, but it's no bubble.

* The blue bars are positive most the time - validating Buffett's point about how value gains a lot more frequently than it shrinks.

Investors who have trouble trusting the stock market should really try to remember the third point. If you stick with stocks long enough, you win. This is because capitalism pushes the businesses that can't grow into extinction, while rewarding those who do grow intrinsic value. Thus, if you own quality businesses or the index as a whole, you eventually make money. Patience is the only requirement.

***

Question: The total value of the stock market compared to GDP is something you look at. If you look at that graph, it's at the highest it's been since the tech crash back in the late '90s. Does that mean we're overextended? Is this a better time to be fearful rather than greedy?

Buffett: I'm buying stocks. But I'm not buying them because I think they're going to go up next year. I'm buying them because I think they'll be worth a lot more 10 or 20 years from now.

My take: Buffett sidestepped directly answering the stock market vs. GDP metric. My guess is he thinks it's a metric to consider, but not a one-dimensional read on whether to buy or sell stocks. No single indicator is.

Also, Buffett doesn't just buy “the stock market.” He invests in individual businesses, which he deems more rationally priced than the index. Even in bear markets, some stocks go up. People forget that.

Buffett also makes clear that he's not timing purchase decisions based on a one or two-year time horizon. He doesn’t expect to have perfect timing, and neither should you.

As a long-term investor, it’s more consequential to get 5-year decisions right, versus being right for 5-weeks or months.

***

Question: You’re sitting on a lot of cash - $110 billion. As a practical matter, don’t we have to have more fear in the marketplace before you’re really deploying a lot of that cash?

Buffett: That creates prices that make me want to shovel out the money as fast as I can. But we’ve been shoveling money out anyway… We keep buying as long as we find something that’s attractive to us.

My take: In this answer, Buffett paints an appropriately nuanced picture.

There are certainly times when it is more advantageous to invest than others. For instance, later in his answer, he cites 2008 and 1974 as some of the best buying opportunities in his lifetime. But those opportunities only come around a few times in an investor’s lifetime.

While today’s prices may not be as good as those, you still have to play the game in front of you. As he says, “you can’t sit around and wait for it, you’re never going to catch the bottom anyway.”

Many people tend to approach investing with a polarized mind. As if there’s only a two-way decision tree, where you pick between being all-in or out. Bullish or bearish.

That is faulty thinking – there’s a ton of room in the middle. It’s important investors find the right zone for them, based on their goals and objectives.

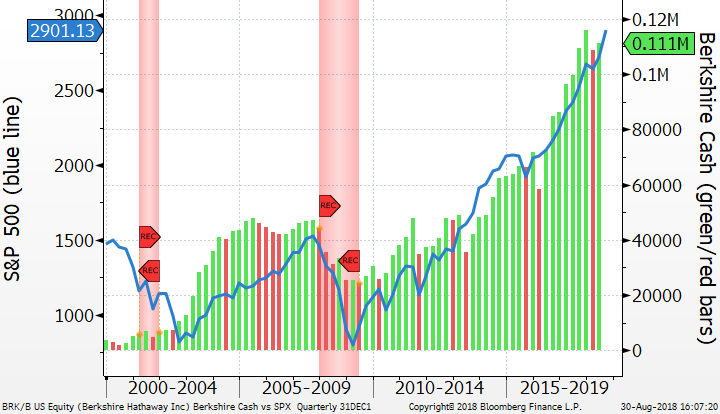

Below is a graph showing Buffett’s cash and cash equivalents at Berkshire Hathaway (bars) overlaid against the S&P 500 (blue line). The bars are green when cash rose versus the prior quarter, and red when Buffett spent down Berkshire’s cash.

Studying this graph, there are several notable takeaways:

* The blue line seldom dips since 2009. When it does, though, you often see red bars. This is because Buffett doesn’t chase the market. As Berkshire’s many businesses drive new cash into the coffer, he prefers to deploy cash during broad market dips. The most recent example was in the first quarter of this year. While the broad market corrected for the first time in a long while, he gobbled up 75 million shares of Apple stock.

* The most red bars appear around 2008-2009. During the recession, Buffett steadily invested into the cascading market. Note: he didn’t pick one quarter, and try to time a bottom perfectly. Rather, he steadily deployed his “dry powder” as stocks became cheaper. Overall, he won by playing offense as the rest of the market went into defense mode.

* Buffett had the ammunition to take advantage of the bear market because he was sitting on a near record cash level in the lead-up to the recession.

While Warren Buffett usually swims countercurrent to the market, countless DALBAR studies show most investors do the opposite. That’s one element that makes Warren Buffett special.

Another factor involves humility. The most celebrated investor of all-time is not out there trying to predict precisely when the next recession will occur, or calling bottoms. He’s always invested to varying degrees. He simply shifts up and down the risk scale gradually, based on the opportunity set.

I try to emulate that with clients I work with by establishing personalized risk zones. We’re never all in cash or short the market. But we become a little more conservative after long bull phases, which provides capacity to be more aggressive when the market eventually goes on sale.

“The less prudence with which others conduct their affairs, the greater the prudence with which we should conduct our own affairs." - Warren Buffett