If there's one thing about which most Americans agree, it's that nobody can be sure what President Donald Trump will do next. One minute he's threatening Iran with apocalyptic destruction; hours later he's touting a two-week cease fire.

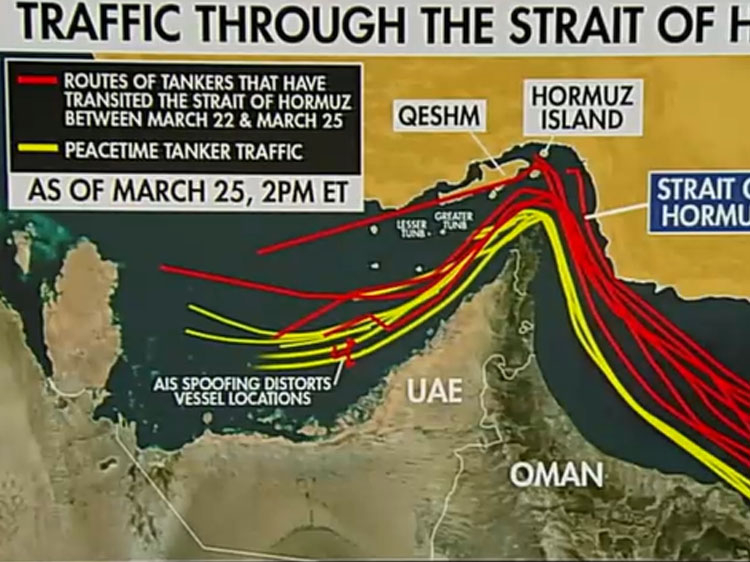

With such uncertainty overhanging the economy, it should come as no surprise that the Federal Reserve’s Open Market Committee held its interest-rate target steady at its most-recent meeting. So did the European Central Bank. And the Bank of England. All three cited the same reason: the escalating hostilities near the Strait of Hormuz had disrupted global energy markets, pushing inflation forecasts higher and making rate cuts too risky.

The Open Market Committee's next meeting will take place at the end of this month, a week after the cease fire is scheduled to expire.

Speaking at Harvard on March 30, Fed Chair Jerome Powell acknowledged that the central bank at its March meeting was merely buying time. "We will eventually maybe face the question of what do do here. We're not really facing it yet because we don't know what the economics effects will be," he said. Meanwhile, markets that had been hoping for relief this summer must wait a while longer.

The Fed and the other central bankers made the right call. Monetary policy can’t open closed shipping lanes or end hostilities between governments. Pretending otherwise would make things significantly worse.

The Hormuz shock was not a monetary problem. It was a structural problem--and will remain so if negotiations between the White House and Tehran prove futile. Then we're back to square one: Oil cannot move through the strait. Tankers are diverting to far-costlier routes. No adjustment to central bank interest rates can alter this reality. Energy costs would spike up again because it has become harder for oil to reach world markets.

When prices rise in response to excessive demand, monetary tightening makes sense. Central banks should restrain inflation when it results from total economic spending (what economists call aggregate demand) growing too quickly. But when prices rise because a war disrupts supply of a crucial input, such as oil, tightening doesn't fix the problem. It merely slows down the rest of the economy to compensate. American families will have to pay more to fill up their tanks no matter what. Artificially depressing demand and risking a recession would make the financial hardship worse. What good is cheaper gas when you’ve lost your job?

This is not a new dilemma. Economists call it a supply shock, and it haunted monetary policymakers throughout the 1970s. When the Organization of the Petroleum Exporting Countries (OPEC) engineered its oil embargo in 1973, the Federal Reserve faced the same basic choice: accommodate the inflation spike and accept price hikes for the foreseeable future, or tighten and risk a recession. The Fed lurched between both, satisfying neither goal, and the stagflation of that decade was the result.

High inflation coincided with meager growth partly because policymakers kept reaching for tools unsuited to the challenge.

So far, we’ve avoided repeating that mistake. But the situation could easily change. If the Iranians close the Hormuz strait again, central banks might lose their nerve and prescribe a disinflationary cure that’s worse than the disease. No good comes from mistaking a supply problem, which central banks can’t control, for a demand problem, which they can.

Most economists advocate “looking through” such shocks, and they’re right to do so. When a price spike is clearly traceable to a temporary supply disruption, rather than to overheated domestic demand, central banks should stand pat.

Monetary policy has inherent limits. Ignoring those limits is how we get high prices and dwindling jobs at the same time.

The U.S. economy took a hit from the oil shock; a demand slowdown on top of that would have meant double the trouble.

This time, Fed Chair Powell, Christine Lagarde, president of the European Central Bank, and their colleagues are off the hook. They are operating reasonably in a very difficult situation. Keeping inflation expectations anchored is important, and given central bankers’ inflationary failures during covid, protecting credibility is more important than ever.

But sometimes credibility requires knowing when not to act. Hence, holding steady in March was the right move.

Instead of monetary policy, the right responses to a supply disruption are themselves supply-side fixes: diplomacy to end hostilities, strategic petroleum reserves to bolster markets, and perhaps diversification to reduce dependence on a single energy source. These are the purview of elected officials — in the United States, Congress and the President — rather than central banks.

The Hormuz shock was a reminder that some economic emergencies require political solutions. Demanding that central bankers handle every conceivable problem would set a dangerous precedent. Let’s keep oil shocks and other supply-side disruptions off monetary policymakers’ plates.