Although there are several, one of the more colorful and dramatic of the eurodollar’s origin stories has to do with Russian dollars. For all kinds of reasons in the fifties, the Soviet Union had accumulated dollar balances with Western banks; including some located or headquartered in the United States. As the Cold War continued to darken, hardened Soviet Communists got cold feet on their money.

Rather than leaving it up to foreign adversaries, the Russians withdrew from US financials and “deposited” their “cash” into largely Western European institutions less likely to go strictly along with any American demands. There was no shortage of countries willing to play in such middle ground.

These were by and large book entries, though, accounts on a distributed ledger which simply kept track of who owed whom what and for how much. And transferring these ledger balances from America to Western Europe could be done by doing nothing more than picking up the phone, or arranging the correspondent bank’s telex message to the respondent.

The eurodollar is, in all its past glories, the combination of those two things. No, not Soviet and dollar, rather offshore and book entry. While it may seem as if this had placed these banks into the very center of the increasingly globalized monetary universe, it was actually the bank network which would reign supreme for all these years ever since.

What’s truly amazing is that way back when, Once Upon A Time, scholars and officials knew this. Monetary competency and even just basic awareness was so much greater fifty years ago than it is today. This is, of course, entirely backward; we love to believe in the ideal of science and how it only ever moves forward, always progressing toward enlightenment and knowledge.

The eurodollar, on the other hand, is a perfect example of the retrograde, reactionary results due from Science™.

Fifty-two years ago, Assistant Penn State Professor Klaus Friedrich both accurately depicted what was then present as well as reached far into the future for the intellectual desert it would become. At that time, the eurodollar system had absolutely exploded, and so naturally interest in it and its explosion followed along.

Yet, Friedrich wrote for Princeton’s Studies in International Finance:

“One of the most striking aspects of the rapidly growing Euro-dollar literature is the fact that so much has been written on the basis of so few data.”

From its very origins, the offshore bank ledger network behind the eurodollar had been steadily and often elegantly solving the world’s primary monetary impediment; what was called Triffin’s Paradox. Basically, the Bretton Woods gold exchange arrangement had been fatally flawed in any condition where international cooperation and trade would greatly increase. So long as it remained minimal, gold exchange could work.

It did not remain minimal for long.

Quite simply, the more the world globalized in trade and finance the more money it would need to keep it all moving. Bretton Woods, however, had fixed the formal reserve currency, the US dollar, in foreign hands to US national reserves of gold. The natural tension between the world’s need for more intermediary money and the stationary reserves behind it, the more it would break down.

The simple solution would be to delink the reserve currency from its national gold holdings. A banking network of bookkeeping entries could accomplish this feat quite nicely (setting aside the hard money arguments against doing this very thing).

Governments around the world, including the US government, once each realized the eurodollar was solving Triffin’s dilemma for them, and how it seemed to benefit everyone, officials remained quiet about it (benign neglect), leaving the eurodollar free to expand both qualitatively as well as quantitatively.

Obviously, to seventies-era scholars, anyway, it had.

As to the qualitative part, it was in experimenting with various forms of transaction money; things like repo or even swaps. In both of those, the very nature of each transaction would undergo radical changes. Back to Klaus Friedrich in 1970:

“A bank in Switzerland, for example, may convert a Euro-dollar deposit into a Euro-sterling claim on a bank in France. The terminal stage of Euro-dollar intermediation in this case is a bank rather than a nonbank borrower.”

National borders matter nothing here; eurodollar is offshore from practically everywhere. Wherever the bank network might be in full working operation, there will be money routes to get done what global commerce and finance demands.

This includes, perhaps counterintuitively given how we’re all taught to think about money from the beginning, the offshore ledger system impacting directly local currencies around the world. That’s what a reserve system can do, and in many cases must do.

A reserve currency has to be the ultimate mediator between often very different national systems. In fact, this is the whole point; to have a single (maybe a couple) currency from which to base both (or multiple) ends of any monetary or credit needs because that reserve currency is common and useful in all places.

Thus, what Professor Friedrich had explained above (Swiss bank going from dollar liability to sterling asset due from a French bank) was the inner workings of this common currency in its natural book entry setting. This sort of elasticity in functioning across all kinds of boundaries, not just geography, is what made the eurodollar so dominant so quickly.

It also placed the banking network beyond the reach of previously silent national authorities. While benign neglect served the world relatively well in its earlier days, by the seventies, you know, Great Inflation.

Once the overseas bank network horses had escaped the national monetary barn, however, there was no turning back. Even in August 1971 when President Nixon “closed the gold window”, he was doing little more than drawing the official curtain down on a Bretton Woods system long since overtaken by far more flexible offshore bookkeeping.

What followed was an almost conspiracy of silence on the subject. Following from Friedrich, while scholarship would remain plentiful throughout the seventies it would all but disappear by the mid-eighties as monetary competency and even interest in money itself dwindled. Officials found it far too difficult to keep track (thus, little data) and then the more time passed it became even more impossible to confess to benign neglect.

Enter Paul Volcker. The myth goes like this: Volcker’s Federal Reserve regained monetary agency to the point his was willing to provoke not one but two nasty domestic recessions in succession (1980 then 1981-82). Such was his monetary resolve in tightening, he would, we’re told, establish for all time Don’t Fight The Fed.

Having demonstrated raw and unchallenged monetary power, the public never has to think about money systems again.

This could not have been farther from the truth, a myth conjured long afterward by a central bank realizing it hadn’t been an actual central bank in a very long time – since around the time the Soviets initiated book entries pulling “dollars” to “deposit” far outside America. I mean, just as a start, the Fed’s jurisdiction ends at the American border.

With a banking network supreme in global money matters, what was the Fed left to do?

Believe it or not, we can turn to Janet Yellen for a square answer. She among her contemporaries has demonstrated a rare willingness to speak close to these very facts. A year before taking Chairmanship from Ben Bernanke, who hardly ever spoke so plainly during his time, a tenure which included, you might recall, the worst global monetary disaster since the Great Depression, Yellen as the Fed’s Vice Chairman acknowledged how the “central bank” truly works:

“The crucial insight of that research was that what happens to the federal funds rate today or over the six weeks until the next FOMC meeting is relatively unimportant. What is important is the public’s expectation of how the FOMC will use the federal funds rate to influence economic conditions over the next few years.

“For this reason, the Federal Reserve’s ability to influence economic conditions today depends critically on its ability to shape expectations of the future, specifically by helping the public understand how it intends to conduct policy over time, and what the likely implications of those actions will be for economic conditions.” [emphasis in original transcript]

If you thought QE was all about money printing and that the US dollar is, you know, the US dollar, Yellen’s self-description of her own job will come as drastic shock.

And should you think her words not clear enough, Ms. Yellen actually follows them by leaving every doubt at the metaphorical monetary door:

“Let’s pause here and note what this moment represented. For the first time, the Committee was using communication–mere words–as its primary monetary policy tool. Until then, it was probably common to think of communication about future policy as something that supplemented the setting of the federal funds rate. In this case, communication was an independent and effective tool for influencing the economy. The FOMC had journeyed from ‘never explain’ to a point where sometimes the explanation is the policy. [emphasis in original transcript]

She was specifically referencing the post-dot-com recession and the Fed’s (limp) response to its aftermath. Make no mistake, sometimes the explanation is the policy” from that time forward – including two-thousand bloody-eight – our so-called central bank dropped the “sometimes.”

Faced with a true monetary crisis, and then its ongoing aftermath, explanation was its only policy. To put it bluntly, the Volcker Myth had itself matured into psychological mumbo jumbo.

This adequately explains pretty much everything from August 9, 2007 onward; not just money, finance, and economy, either, also gross distortions in politics along with snowballing social upheaval.

This is how we begin 2022 with Russia invading Ukraine and the world’s public (and very likely the vast majority of its politicians) believing the US government controls the US dollar through nothing more than SWIFT and thus holds some substantial influence over Vladimir Putin’s decision-making.

This isn’t just a gross oversimplification; it is an outright falsehood designed, in a big picture sense, to further perpetuate the Volcker Myth (along with puffing up the optics of the near-term political response).

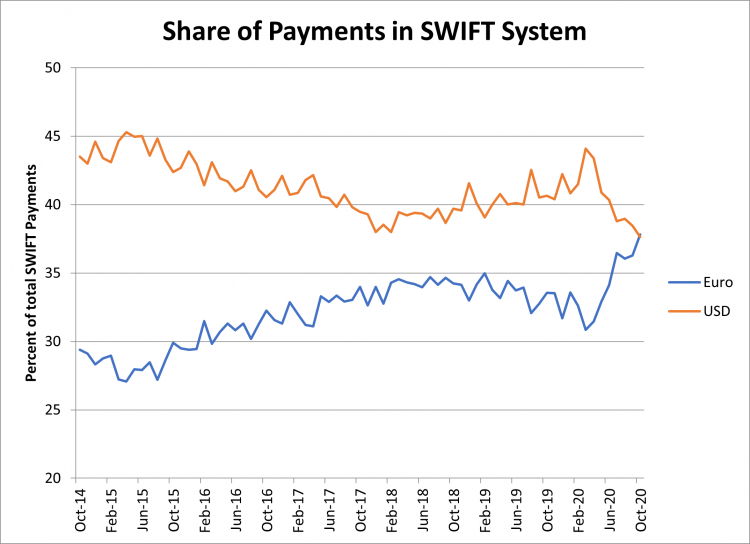

In truth, SWIFT is little more than one messaging service, fifty-year old technology (sure, it’s been updated over the years but not nearly as much as you might think) that came immediately after those old telexes. SWIFT constitutes very little insofar as the inner workings of the offshore banking network is concerned.

We’re left with the same false impression that the dollar is under control of the US government and its various agencies, and they can wield supreme power at the touch of a button.

It hasn’t been this way, ironically, since the first time the Russians feared confiscatory retaliations (this is by no means a defense for Russia, then or now; reciting facts doesn’t constitute “taking sides”).

The downside to all this monetary misunderstanding in 2022 isn’t limited, of course, to Eastern European settings. You’re probably well aware of how the Federal Reserve is today primed for rate hikes to begin in a couple weeks. After all, they’ve been communicating these for months already.

What was it that Yellen said eight years ago?

“…what happens to the federal funds rate today or over the six weeks until the next FOMC meeting is relatively unimportant.”

Couldn’t agree more, if for all the opposite reasons. My view is joined by the entirety of the global offshore banking network, too. We know this because, though there still isn’t any eurodollar data, and the once-burgeoning eurodollar scholarship has almost entirely disappeared, ledger transactions flow through US$ market tapes anyway and they aren’t difficult to decode and interpret.

The eurodollar futures market, for one, only echoes more and more how the federal funds rate today or over the next week is indeed largely irrelevant. As that curve inverts more and more (up to 30 bps upside down as I write), it is an increasingly confident bet against the Fed’s intentions, more specifically the reasons behind them.

And while it would be easy to attribute to Russian aggression such doubt and skepticism as to the Federal Reserve expectations for inflation and overheating economic growth, this particular set of signals – corroborated broadly by all manner of consistent money indications – long predates the current hot war conflict. Eurodollar futures inversion first showed up on December 1, having set in motion from way back last October.

The explanation for why this could be is the same one as why asking global banks (the US government controls nothing) to exclude up to ten Russian banks from SWIFT is barely an inconvenience for any of them: the offshore ledger money system.

Deprive some of Russia’s institutions their ability to message to correspondents using SWIFT and they’ll simply communicate (how’s that for more irony!) with them some other way (including just picking up the phone) because the offshore correspondents are still there. They will continue to conduct their monetary business regardless of the method payments requests are sent and received.

But the overall amount of “money” that becomes available to be sent and received, that’s a function of aggregate bank conditions within it regardless of central bank communications.

The Fed fears inflation and overheated growth, so it communicates a steady series of rate hikes ahead. The monetary ledger is not inflationary and is being priced far more likely to lead to more disinflation if not worse, and so it more forthrightly prices against the rate hike series.

The world is just this upside down, in more ways than should be imaginable, because Economics hasn’t followed scientific principles that Mr. Friedrich had urged so very long ago. Rather, Economics preaches Science™ which tries to trick you into not thinking about the most important factors of the last half century. This whole Russia/SWIFT debacle is merely the latest example of just how effective it has been, in terms of maintaining the public’s as well as its own monetary ignorance.

Insofar as fixing this, well, an assistant Penn State professor had given us the answer fifty-two years ago. Damn right, democracy dies in darkness. But in whose shadow?